Exclusive ULI Fall Conference Release: The Investors’ Guide to 2024 Real Estate [Part 1]

Smart Capital Center had the opportunity to engage with industry leaders at the ULI Fall Meeting in Los Angeles. Amidst the many discussions, one stood out: the “Emerging Trends in Real Estate® United States and Canada 2024″ report. Presented by Chuck DiRocco, Director of Real Estate Research at PwC, this report was all about the…

Written by

Smart Capital Center had the opportunity to engage with industry leaders at the ULI Fall Meeting in Los Angeles. Amidst the many discussions, one stood out: the “Emerging Trends in Real Estate® United States and Canada 2024″ report.

Presented by Chuck DiRocco, Director of Real Estate Research at PwC, this report was all about the “Great Reset” that signals a shift, with enduring high-interest rates and economic uncertainty ahead.

This new era redefines office spaces and investment strategies, emphasizing the need for adaptability in commercial real estate. With borrowing costs rising and likely to remain high, making informed decisions is more critical than ever.

To give you a comprehensive understanding, we will present these insights in two parts. In the first part, we’ll delve into five key trends that are shaping the real estate sector in 2024. These trends will guide your strategic decisions and operational plans in this evolving market.

In the second part, we’ll explore the other five trends, highlighting the opportunities that emerge in this transformative landscape.

Real Estate Outlook: The 10 Trends to Watch

1. Expect Long Periods of High-Interest Rates

A recession is inevitable in the economy. Industry experts believe the economy is headed for a “soft landing” or a “growth recession”. This scenario would feature a strong labor market and decent job growth. However, the current interest rates are pushing the economy towards a slowdown.

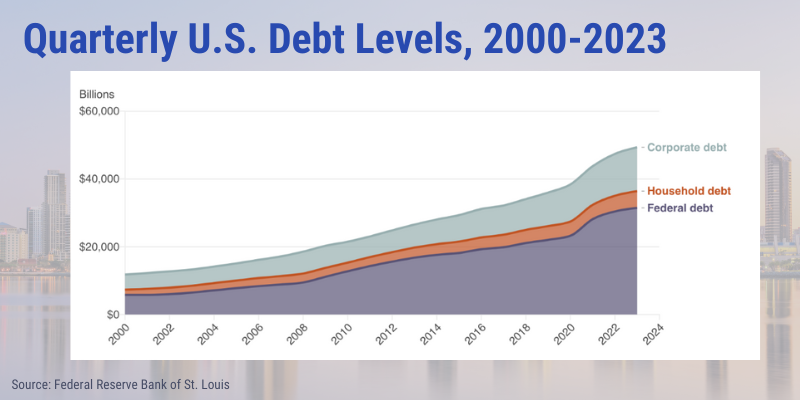

Economic resilience is apparent with a 4.9% rise in GDP, yet debt issues remain. The national deficit has reached 1.4 trillion USD and the federal debt-to-GDP ratio is a concerning 220%. Increasing interest payments are undermining investor confidence and reducing the purchasing power of dollar.

DiRocco noted, “On the corporate debt side, it’s all about financial stability, being able to meet debt obligations.” This is evident in recent strong third-quarter earnings influenced by inflation.

The focus is now on future financial guidance. Personal debt has also surged, now accounting for a significant portion of the GDP at 70%, or $13 trillion. This increase, driven by pandemic-era spending, has led to reduced savings rates and heightened consumer risk management.

Commercial real estate, on the other hand, particularly the office sector, is facing a critical moment with $5.6 trillion in debt. As these debts mature, particularly the $2.8 trillion due by 2027, refinancing or extending loans will become more complex due to higher interest rates, decreased property values, and changing lease agreements.

DiRocco also pointed out, “The concern about office space, with $750 billion in the spotlight and in the media, is significant. Looking forward, $2.8 trillion of this debt will mature by 2027, with half being held by banks. Considering these deals were made a decade ago in 2015 at interest rates of around 2 to 2.25%, compared to nearly 4.9% now, managing these loans is a key issue.”

Regarding loan refinancing or extension, he explained, “For either option, you will need more equity as values have likely declined. Additionally, you will need more loan collateral. Consider the leases that may have rolled over, especially as people are using less space or have vacated the building, which means you’ll need more capital.”

Economists, however, remain concerned. Soft landings are rare and challenging, with economies more susceptible to shocks as they slow, which can lead to a full recession. Past experiences, such as the Global Financial Crisis, have shown that optimistic projections of a soft landing often fail in the face of unforeseen events.

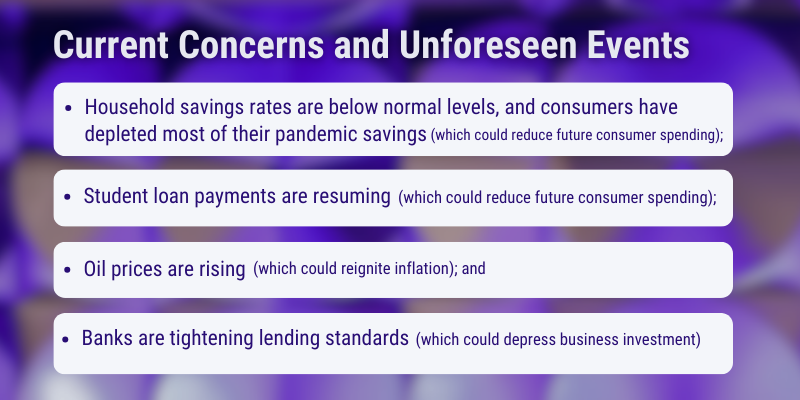

Current concerns include:

- Household savings rates are below normal levels, and consumers have depleted most of their pandemic savings (which could reduce future consumer spending);

- Student loan payments are resuming (which could further reduce consumer spending);

- Oil prices are rising (which could reignite inflation); and

- Banks are tightening lending standards (which could depress business investment)

Inflation has decreased from its peak but reducing it to the 2% target is proving difficult. In August 2023, consumer prices surged at their highest rate in over a year, highlighting the challenge of curbing inflation completely.

While wage growth has been strong, benefiting lower-income workers in particular, it complicates efforts to control price inflation.

Inflation remains above the Federal Reserve’s target rates, raising concerns that policymakers might increase rates to a level that could lead the economy into recession. There’s also the risk that the Federal Reserve might maintain high rates for too long, as the impact of rate hikes is often delayed.

Leaders in the Commercial Real Estate (CRE) industry, however, are optimistic about achieving a soft landing. They see that the economy is expected to continue growing, albeit at a slower pace, with sustained high-interest rates. The Federal Open Market Committee anticipates a slowdown in real GDP growth to 2% in 2023, decreasing to 1.5% in 2024, and then slightly increasing in the following years.

Despite this anticipated slowdown, the period of higher interest rates is likely to persist. The inflationary pressures are expected to be more significant than in the past two decades, which were characterized by deflationary trends due to free trade.

2. Increased Competition for CRE Funds in Capital Allocation

For years following the Global Financial Crisis (GFC), commercial real estate (CRE) experienced exceptional returns, driven by strong rent growth, decreasing capitalization rates, and rising property values, largely fueled by near-zero interest rates. This trend experienced a brief setback during the COVID lockdown, only to rebound in 2021, strengthened by high warehouse and apartment rents and robust investor demand.

However, this upward trajectory was paused in March 2022 when the Federal Reserve implemented the first of eleven rate hikes. This shift significantly altered the market, diminishing the attractiveness of CRE as an investment. Previously, CRE was favored for its yield, income growth, inflation protection, and security of tangible assets.

Now, with 10-year Treasury bond yields surpassing 4.5%, other assets present more attractive risk-adjusted returns, leading to increased competition for CRE funds in capital allocation. This new investment environment challenges the previously rational aggressive exit strategies and optimistic future betting that had characterized the industry for the last 15 years.

The industry is also bracing for the “higher for longer” interest rate era. This signals challenging adjustments for the real estate industry, marked by increased borrowing costs that hinder acquisitions and new construction.

This environment has led to a decline in transaction activities and building projects, as investors, still accustomed to the previous era of zero interest rates, struggle to adapt to the new norm. Additionally, the industry faces prospects of slower income growth, influenced by declining population growth due to lower birth rates and stricter immigration policies, and subdued economic expansion, partly attributed to these higher interest rates.

These factors result in slower job creation, reduced space demand, and decelerated rent increases. Consequently, capitalization rates are expected to rise to align with these new realities of lower growth and higher costs, leading to a decrease in property values and shifting the negotiating advantage towards buyers, especially in highly leveraged property markets.

The adjustment to the new economic reality in the real estate sector is expected to be a prolonged process. Many property owners, lacking a pressing need to sell, are hesitant to engage in transactions, reducing market activity in the short term.

However, as acceptance of the current macroeconomic conditions grows, those needing to sell may gradually enter the market. Certain owners, particularly those facing lease or debt expirations, might be compelled to sell due to unfeasible refinancing options or inability to meet new banking requirements, such as higher equity contributions or maintaining bank deposits.

Despite this, the level of distress in the market remains relatively low, although some owners are beginning to recognize the diminishing demand and prices, especially in the office sector, where some have abandoned prime properties.

While these value losses are significant, they are often not catastrophic, especially for assets held over a longer period, as the overall decline in property values is modest compared to the gains seen since the GFC.

However, certain sectors are confronting more serious challenges. Notably, the office market has seen a decline, with values reportedly down by over 30%, and a further decrease is anticipated. This situation necessitates that many office owners will soon face critical decision points.

Additionally, recent investments in apartments and industrial buildings based on optimistic future rent and cap rate projections are facing challenges too. This situation, although not widespread, indicates a need for further property value adjustments to catalyze the next wave of investments in a landscape characterized by higher interest rates and slower growth.

The commercial real estate industry, diverse in both property types and geographic locations, is experiencing varied impacts in the current economic climate. While the office sector significantly influences the perceived risks and opportunities, fundamentals in most sectors remain strong, with continued investor interest, particularly in well-located industrial and multifamily properties, data centers, student housing, and medical offices.

In this complex environment, Smart Capital Center offers an AI-powered platform that enables investors to navigate these challenges effectively. Leveraging automation and deep market and deal insights, the platform helps investors make informed decisions in a landscape marked by cautious investment strategies and a reevaluation of asset values.

3. Remote Work Reshapes Office Demand

The office sector of CRE is undergoing significant changes due to evolving work practices. The shift towards hybrid and remote work has led employees to make substantial investments in their home offices and adjust their lifestyles, with many moving to distant suburbs or adopting more flexible work schedules.

Despite attempts by some companies to mandate a return to the office, data shows only a marginal increase in office occupancy post-pandemic, with industry data indicating that tenant demand for office space has significantly decreased to about 60-70% of pre-pandemic levels. This reduction in demand has led to an excess of office space, and unlike apartments, where lowering rent can attract tenants, some obsolete office buildings may not find tenants even at reduced rents.

While premier, newer office buildings continue to attract significant leasing interest, and office markets in smaller metro areas are managing relatively well, the general scenario in major markets is less optimistic. There, especially in class A downtown spaces, office occupancy rates have drastically fallen, and vacancy rates have soared, outpacing those in suburban areas. This decline is particularly concerning in the country’s leading office markets, where vacancy rates have more than doubled since the pandemic, despite a record high in knowledge-based employment, which traditionally drives office demand.

While some draw parallels between the recent rebound in the retail sector and the potential for a similar recovery in the office sector, the overall outlook remains cautious. The possibility of an office sector revival is likened to a slim chance. Despite this, there are industry optimists. Some executives note encouraging signs, such as larger technology companies acknowledging lower productivity in remote work settings.

4. Reduced New Loan Origination. Increased Outstanding CRE Debt

Debt is vital to the functioning of not only commercial real estate markets but to the economy as a whole.

The availability of credit has become a significant challenge since the Federal Reserve started raising interest rates in March 2022. This has been a key factor in the decline of real estate sales transactions, as debt is crucial for most investors. The industry is grappling with not just reduced availability of debt but also higher financing costs.

The Mortgage Bankers Association (MBA) reports that loan origination volumes in 2023 have decreased by about 30% from the average in the first half of the years 2016–2019, a drop greater than the 24% decline in sales transactions during the same period.

This decline in originations spans across all major debt sources, including banks, commercial mortgage-backed securities (CMBS), and life insurance companies, though private debt sources are occasionally filling the gap. Despite the perception of undersupply in debt for acquisitions and refinancing, CRE mortgage debt increased by 7.8% year-over-year as of August 2023, which is more than double the increase in household and corporate debt. This contrast highlights the unique challenges facing the CRE sector compared to non-CRE businesses, where a study reports that most small businesses find their approved credit adequate for their needs.

The paradox between the decline in new loan originations and the increase in outstanding CRE debt is explained by banks issuing fewer new loans while borrowers retain their existing lower-cost debt. This situation has led to a rise in the total volume of outstanding CRE debt, reflecting the challenges of accessing new credit at higher interest rates. Developers note that not only has credit become more expensive and scarcer, but it is also subject to stricter underwriting standards, as indicated by data from the Federal Reserve Bank of Dallas.

The real estate industry is facing a potential liquidity crisis due to the reduced availability and increased cost of debt. Investors and developers are finding it challenging to acquire new assets or undertake new projects, leading some to rely more on cash reserves and delay financing.

A critical issue is the large volume of commercial and multifamily mortgages maturing soon – over $725 billion in 2023 and $1.2 trillion in the following two years, representing a significant portion of the total outstanding CRE mortgages. Much of this debt will be subject to higher refinancing rates, forcing some lenders to negotiate extensions under the “extend and pretend” approach.

Additionally, owners who recently purchased assets with optimistic rent growth and cap rate assumptions are now facing higher interest rates and lower loan-to-value ratios, making it difficult to refinance their debts without injecting additional equity. This situation leads to decreased asset values and potential defaults, especially in the multifamily sector. The outlook is even more challenging for owners of underperforming assets, particularly major office buildings, which were acquired under more favorable pre-pandemic conditions and are now struggling with tenant departures and the need for significant capital investments. Some owners are opting to default on their debts and surrender their properties to lenders.

Currently, delinquency and default rates in the CRE sector remain relatively low but are gradually increasing, especially in CMBS, life insurance companies, and banks and thrifts. This trend is expected to intensify, particularly in the office and multifamily sectors, as major leases and mortgages approach expiration. Although this situation is challenging for affected borrowers and lenders, it may benefit investors by increasing sales transactions and bringing much-needed pricing transparency to the market.

However, the process is not straightforward. With many properties expected to hit the market due to the inability of owners to refinance, significant repricing is anticipated, and there may not be enough capital available to cover the gap, leading to widespread distress. This environment presents opportunities for private lenders, as the retreat of traditional lenders opens the door for them to engage with higher-quality borrowers and obtain better rates. Nonetheless, the overall outlook for many CRE lenders is grim, with abundant opportunities for new loans contrasted by difficulties in existing portfolios.

In the current challenging time for the CRE sector, marked by a decrease in loan originations and an increase in outstanding CRE debt, Smart Capital Center offers crucial support to investors. SCC alleviates these challenges by helping get better property and market insight and cut transaction costs by leveraging automation and data at every step of the investment and financing lifecycle.

5. Eco-Anx Climate Change Impacts Property Investments

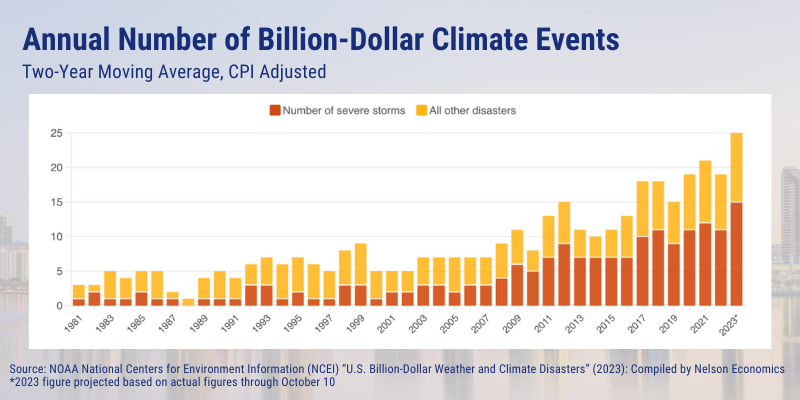

The year 2023 is shaping up to be one of the hottest years on record, with a global average surface temperature for June through August significantly above the 30-year average. This increasing frequency and intensity of climate events directly impact the real estate sector, as the quality and financial performance of real estate assets are becoming more closely tied to their sustainability performance.

This situation presents complex challenges for investors and fund managers, who must navigate a range of issues including decarbonization, energy efficiency, indoor environmental quality, increasing insurance costs, reduced insurance availability, and uncertain access to essential resources such as power and water. These challenges underscore the growing importance of sustainable practices in the real estate industry.

The increasing urgency of climate-related risks and their impact on property investments highlight a significant industry challenge known as “the tragedy of the horizon.” This concept, coined by former Bank of England governor Mark Carney, refers to the discrepancy between the short-term decision-making horizons of most market participants and the longer-term nature of climate change risks.

While enhancing a building’s resilience to climate events makes financial sense over its lifespan, the perceived risk of such events within the typical investment hold period is low, leading many owners to rely on insurance to cover potential damages. This approach, however, overlooks the long-term risks and costs associated with climate change. The industry’s tendency to focus on short-term gains and decisions, as noted by a leading CRE academic referencing Daniel Kahneman’s work, results in market capitalization not fully reflecting the risks posed by climate-related events such as fires and floods, creating a significant disconnect between investment strategies and the reality of climate change impacts.

Insurance, traditionally a minor expense for commercial property owners, has seen costs more than double in recent years, significantly impacting property owners. This surge in insurance premiums is causing concern among owners who are accustomed to passing these costs to tenants but now face the risk of tenant resistance or constraints on future rent increases.

In some high-risk areas, insurers are choosing to withdraw coverage altogether, partly due to regulatory limits on premium increases. Property owners are thus confronted with the choice of either accepting the high insurance costs reflective of the perceived risk or opting to self-insure. This challenge is particularly acute for smaller investors in high-risk regions, where securing insurance is increasingly difficult, potentially affecting their ability to obtain long-term mortgages.

The overall result is a likely reduction in new supply of housing or industrial space in high-risk areas, such as coastlines or near forests, and consequently higher rents in these sectors. This trend highlights the growing need for CRE investors to explicitly address climate-related risks in their investment strategies.

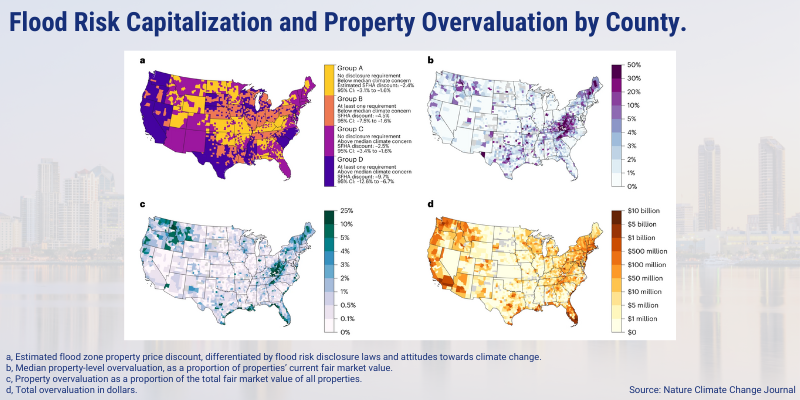

Residential real estate is facing significant challenges in addressing climate risks, primarily due to a lack of awareness and information among homeowners. A Fannie Mae survey revealed low awareness of flood risks, especially among those in high-risk zones, with many not having adequate insurance. This issue is exacerbated by outdated FEMA flood maps that don’t reflect future climate change risks and resistance to updating them due to potential property value impacts.

Additionally, subsidized flood insurance often underprices risk, leading to inadequate preparation for long-term climate threats. Despite these risks, studies show that migration into flood-prone and wildfire-prone areas is increasing. A study in the journal Nature indicates that residential real estate markets are failing to incorporate flood risks into property valuations, potentially overvaluing the market by billions. Furthermore, a Redfin study suggests that as homebuyers become more aware of flood risks, property values in high-risk areas could decline.

This emerging awareness and valuation adjustment, while currently focused on residential markets, could likely extend to commercial real estate, as both sectors are subject to similar climate forces and evolving consumer perceptions, underscoring the principle of “buyer beware.”

That wraps up the first half of our deep dive into the trends reshaping the real estate industry. Continue reading the second half of this blog to discover the remaining trends that are equally crucial for influencing your strategic decisions in this dynamic market.

Discover how Smart Capital Center can drive speed, enhance insight, and cut costs for any real estate transaction. 🚀🚀🚀

or contact us at demo@smartcapital.center or call (866) 725 – 0555

Smart Capital is the world’s first real-time valuation and mortgage platform. It empowers real estate investors with institutional-grade insight, unbiased investment analysis, ultra-fast property valuation & deal underwriting, low-cost transaction support, free portfolio monitoring, and capital to enable smart investment decisions and fast dealmaking.

Discover how Smart Capital Center

- Drives speed

- Enhances insights

- Cut costs

Across full investment and Financing lifecycle

Recommended

All Articles

Thank you!

Your message has been successfully sent.

Have a nice day!